Do You Need a Tax Audit? A Guide for SME Owners

Many small and medium business owners are unsure whether a tax audit applies to them. The confusion usually starts when turnover increases, digital payments rise, or presumptive taxation comes into play.

Tax audit rules are not complicated. But they are often misunderstood.

This guide explains tax audit limits for SMEs in India in clear terms. By the end, you should be able to answer one simple question: Do I need a tax audit this year or not?

Key Insight

A tax audit is a compliance requirement, not a penalty. It becomes mandatory when your business crosses certain financial thresholds defined under Section 44AB of the Income Tax Act.

What Is a Tax Audit Under the Income Tax Act?

A tax audit is a review of your business or professional accounts from an income tax perspective.

It is conducted by a Chartered Accountant under Section 44AB of the Income Tax Act, 1961.

Verification Purpose

A tax audit helps the Income Tax Department verify whether books of accounts are properly maintained and income/expenses are correctly reported.

Verification Reporting Requirements

The findings are reported using Form 3CA/3CB and Form 3CD, which contains detailed disclosures about your financial transactions.

Compliance, Not Penalty

A tax audit does not mean wrongdoing. It is a compliance requirement once certain limits are crossed as your business grows.

Why Is Tax Audit Mandatory for Some Businesses?

The main objectives of a tax audit are:

Accurate Reporting

To ensure accurate reporting of income and reduce errors, omissions, and incorrect claims.

Transparency

To improve transparency in financial records and build trust with tax authorities.

Efficient Assessment

To make income tax assessments smoother and faster for both taxpayers and the department.

For SMEs, a tax audit often acts as a checkpoint when the business starts growing. It’s a sign that your business has reached a significant size where formal verification becomes necessary.

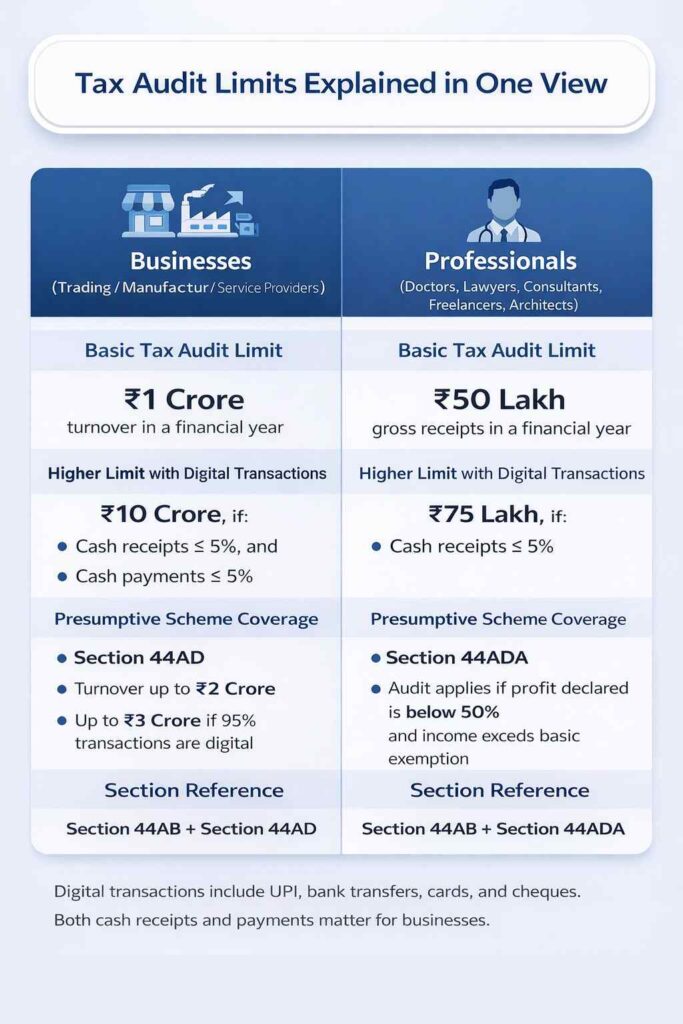

Tax Audit Limits for Businesses Under Section 44AB

Understanding the exact thresholds is crucial to determine if your business needs a tax audit.

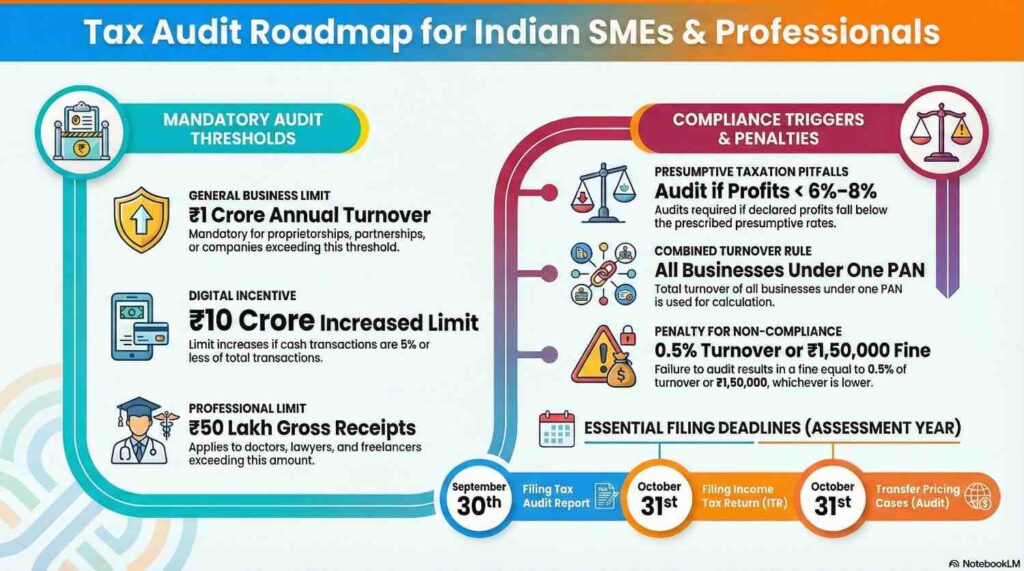

General Turnover Limit

₹1 Crore

A tax audit is mandatory if total sales, turnover, or gross receipts exceed ₹1 crore in a financial year.

Applies to: Proprietorships, Partnerships, LLPs, Private limited companies.

Digital Transaction Limit

₹10 Crore

The limit increases to ₹10 crore if cash receipts & payments each stay below 5% of total transactions.

Condition: At least 95% of transactions must be digital or banking-based.

Professionals Limit

₹50 Lakhs

For professionals (doctors, lawyers, consultants, etc.), tax audit is mandatory if gross receipts exceed ₹50 lakh.

Note: Based on gross receipts, not net income.

Multiple Businesses Under One PAN: If a taxpayer runs more than one business, the combined turnover of all businesses is considered. Even if one business is small, audit applies if the total exceeds the limit. This is often overlooked by SME owners.

What Counts as Digital Transactions?

Bank Transfers

UPI Payments

Cheques

Credit Cards

A common mistake is assuming that using UPI alone is enough. Both receipts and payments must stay within the 5 percent cash limit to qualify for the higher ₹10 crore threshold.

Presumptive Taxation Schemes and Audit Applicability

Presumptive taxation schemes simplify tax compliance for small businesses and professionals, but they come with specific audit triggers.

Presumptive Taxation for Businesses

Small businesses can opt for presumptive taxation if:

- Turnover does not exceed ₹2 crore, or

- Up to ₹3 crore if 95% of transactions are digital

Presumed Profit Rates:

- 8% profit is assumed for cash receipts

- 6% profit is assumed for digital receipts

When these conditions are met, tax audit is not required.

Presumptive Taxation for Professionals

Professionals opting for presumptive taxation under Section 44ADA can avoid audit if:

- They declare at least 50 percent of gross receipts as income

However, a tax audit becomes mandatory if:

- They declare profits below 50 percent, and

- Their total income exceeds the basic exemption limit

When Audit Becomes Mandatory Under Presumptive Taxation

A tax audit is required if:

- The business declares profit lower than the prescribed percentage, and

- Total income exceeds the basic exemption limit

Audit is also mandatory if:

- The business opts out of Section 44AD after opting in, and

- This happens within the 5-year lock-in period

Important: Once opted out, the business cannot re-enter the scheme for five consecutive assessment years.

Need Help with Presumptive Taxation?

Our experts can guide you on whether presumptive taxation is right for your business and help you avoid unexpected tax audit triggers.

Important Considerations for SME Owners

Tax Audit in Case of Business Loss

Incurring a loss does not automatically exempt a business from tax audit.

Tax audit is mandatory if:

- Turnover exceeds ₹1 crore, even if there is a loss

- The business is not under presumptive taxation

For businesses under presumptive taxation:

- Audit may not apply if income remains below the basic exemption limit

Loss cases are frequently misunderstood and should be reviewed carefully with a CA.

Due Dates & Penalties

| Task | Due Date (Assessment Year) |

|---|---|

| Filing Tax Audit Report | September 30th |

| Filing Income Tax Return (ITR) | October 31st |

| Transfer Pricing Cases | Oct 31st (Audit) / Nov 30th (ITR) |

Penalty for Not Conducting a Mandatory Tax Audit

If a required tax audit is not completed, the penalty under Section 271B is:

- 0.5 percent of turnover, or

- ₹1,50,000, whichever is lower

Common Mistakes SMEs Make

- Assuming digital payments automatically remove audit requirements

- Ignoring combined turnover from multiple businesses

- Declaring lower profits under presumptive taxation without checking audit triggers

- Missing audit deadlines due to late planning

- Not maintaining proper documentation to support reasonable cause claims

Most penalties arise from misunderstanding, not intent. Proactive planning with a Chartered Accountant can help avoid these common pitfalls.

Quick Checklist: Does Tax Audit Apply to You?

Ask yourself these questions to determine if your business needs a tax audit:

Tax Audit Eligibility Checklist

Is your turnover above ₹1 crore or ₹10 crore with digital compliance?

Remember: The ₹10 crore limit applies only if cash transactions are below 5% of total.

Are you a professional earning above ₹50 lakh?

This includes doctors, lawyers, architects, engineers, consultants, and freelancers.

Have you opted for presumptive taxation?

If yes, ensure you're declaring profits at or above the prescribed rates to avoid audit.

Are you declaring lower profits than prescribed under presumptive taxation?

This is a common audit trigger that many businesses overlook.

Do you run multiple businesses under one PAN?

The combined turnover of all businesses is considered for audit applicability.

If the answer to any of these is yes, a tax audit may apply to your business. Consult with a Chartered Accountant for a definitive assessment based on your specific circumstances.

How a Chartered Accountant Helps SMEs With Tax Audit

Working with a qualified Chartered Accountant can simplify the entire tax audit process and ensure compliance.

Correct Assessment

Assess audit applicability correctly based on your specific business structure, transactions, and financial thresholds.

Documentation Guidance

Assess audit applicability correctly based on your specific business structure, transactions, and financial thresholds.

Accurate Filing

Prepare and file audit reports (Form 3CA/3CB and Form 3CD) accurately and within deadlines.

Penalty Protection

Help avoid penalties, notices, and legal complications by ensuring full compliance with tax laws.

Early review always reduces last-minute stress. Don’t wait until the deadline approaches. Consult with a CA at the beginning of the financial year to plan accordingly.

Need Professional Tax Audit Assistance?

Our team of experienced Chartered Accountants can help you navigate tax audit requirements, ensure compliance, and avoid penalties.